Barbers are making more money than ever—thanks to the growing demand for trendy hairstyles and sharp beards. Even clients are willing to pay top dollar for the best.

If you’ve got the skills, you’ve got the opportunity to earn big.

But skill alone won’t keep your barbershop running. It’s still a business, and if you don’t manage your finances right, you could struggle—even with a packed shop. High costs, bad pricing, and poor planning can eat away at your profits.

That’s where you need a solid financial plan to ensure your barbershop stays profitable.

Not sure how to create a plan?

Worry not; this guide will walk you through everything you need to know, step-by-step!

How do you build barbershop financial projections?

Creating realistic financial projections for your barbershop involves thorough analysis and meticulous planning to comprehend its financial health and growth potential.

Here’s a step-by-step guide to help you build accurate and actionable projections while ensuring you factor in every detail:

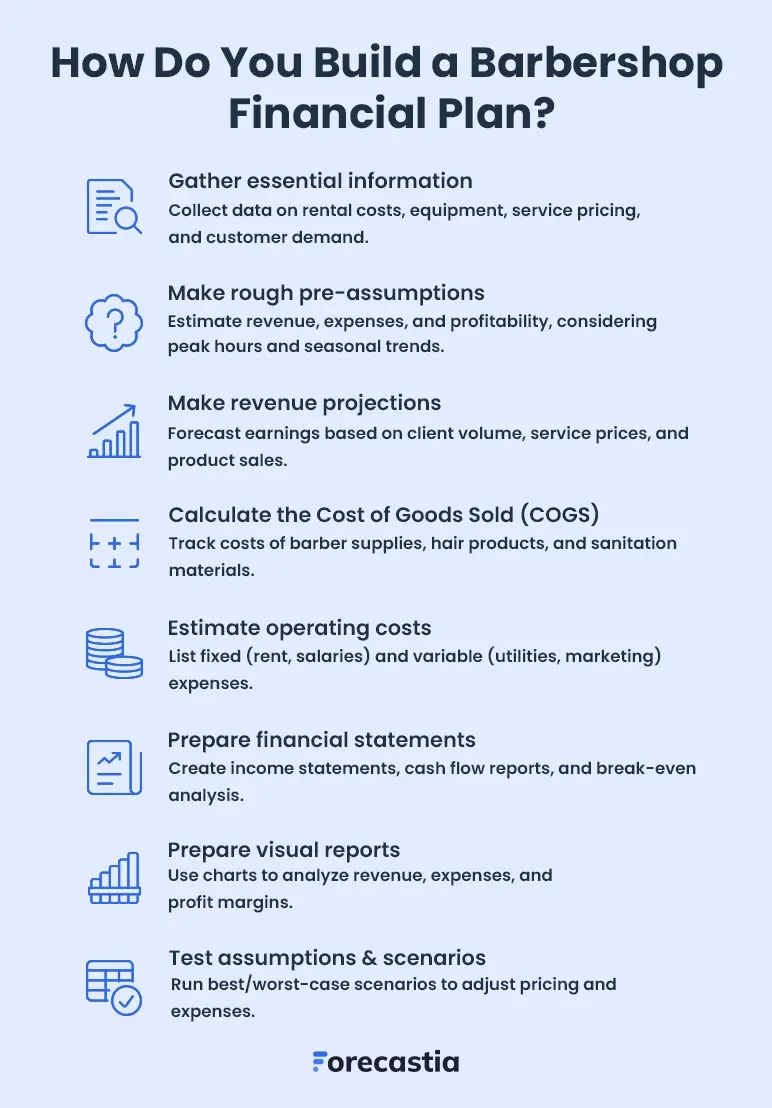

1. Gather essential information

First, collect all the relevant key data that lays the groundwork for accurate financial projections.

This would include your barbershop details like:

- Current operations

- Target demographics

- Historical financial performance

- And industry benchmarks.

Start with your barbershop’s sales data—check daily and weekly earnings, busy hours, and seasonal trends. If you're just starting, look at market trends, industry benchmarks, and local competitors to make smart estimates.

Further, understand your customers inside out.

- Who are they?

- What styles do they prefer?

- How often do they visit for a cut or shave?

Then, track inventory data—monitor stock levels (of shampoos, clippers, razors, and styling products), turnover rates, and supplier costs to ensure precise cost calculations.

Most importantly, don’t forget to evaluate the past performance data of your barbershop to understand what drives your business.

Consider analyzing previous revenues, costs, and profits to detect trends and highlight the areas for improvement. Check how some of the marketing campaigns, service packages, or seasonal changes impacted your sales and cost.

That’s how you'll have everything you need to create accurate and actionable financial projections.

2. Make rough pre-assumptions

Now, make some preliminary assumptions for your barbershop’s financial projections based on gathered data. Such estimates will outline your business's revenues, expenses, and profitability levels.

Start by focusing on the basics: How much you’ll make in monthly revenue, how much customers will spend on average, and what your operating costs might look like.

Use the understanding of past sales trends, industry benchmarks, and your own research. Even, take into account factors like seasonal changes, new haircut styles or upcoming services that could affect your numbers.

Here are a few key metrics to consider while making your assumptions:

- Revenue growth: Predict a percentage increase in sales, such as a 5% annual growth based on an expanding customer base or marketing efforts.

- Cost increases: Plan for rising product costs, rent, or wages, like a 10% spike in utilities during peak seasons.

- Seasonality: Factor in holiday rushes when people want fresh cuts and slower months like January when demand dips.

- Economic conditions: Account for inflation, rising wages, or other economic factors that may impact both costs and customer spending power.

Don’t aim for perfection—these are rough estimates to guide your planning that will evolve over time. So, revisit them periodically as actual data comes in.

3. Make revenue projections

Revenue projections are all about figuring out how much money your barbershop might make.

To get started, think about a few simple things: How many seats you have, how often customers turn over, and how much they usually spend.

Breaking it down step-by-step makes it easier to see your earning potential.

For example, if your shop has 5 chairs, serves 10 clients per chair daily, and the average service costs $25, the math looks like this:

5 chairs × 10 clients × $25 × 30 days = $37,500/month

But, you’ll also need to consider things like holidays, weekends, or special events—they can bring in more people and boost your revenue even further. On the other hand, slower months or weekdays might drive less income.

Additionally, consider other ways to increase revenue. Services like premium grooming packages, beard treatments, retailing hair products, or offering memberships and loyalty programs can add a significant boost to your overall earnings.

By including these extra streams, you’ll get a more accurate picture of what your barbershop can earn.

Revenue projections aren’t merely a dry exercise of crunching numbers—they set realistic expectations while preparing for both the busy times and the quieter ones.

4. Calculate the Cost of Goods Sold (COGS)

The next step is to calculate your Cost of Goods Sold (COGS)—basically, the direct costs of providing your barbering services. For this, it would include your shampoos, styling products, razors, and other items that are directly used in your services.

Here's an easy way to do your COGS calculation:

List your supplies: Write down everything used in your services, including shampoos, conditioners, styling products, razors, blades, disinfectants, and towels.

Find the costs: Check invoices and receipts from suppliers to see how much you’re spending on products and supplies.

Calculate per service: Figure out how much each haircut or grooming service costs you. (i.e. If a haircut requires $2 worth of shampoo, gel, and blades and you handle 500 haircuts a month, your COGS for haircuts is $1,000).

Add it up: Total the cost for all services to get your monthly COGS.

For example, if your barbershop makes $30,000 in a month but spends $5,000 on supplies, then $5,000 is your COGS.

Knowing your COGS will help you manage expenses, optimize resources, and boost profits.

boost profits.

5. Estimate operating costs

Next, describe the expected expenses incurred to operate your barbershop.

When assessing the business operational costs, first list the fixed costs that would remain the same month in and out, including rent, insurance, and salaries.

Then, you have to identify variable costs that vary over time. It includes utilities, hair care products, or marketing expenses.

Lastly, sum up the fixed and variable costs to come up with your total operating costs.

Let’s say your barbershop has these monthly costs:

- Rent: $3,000

- Utilities: $1,000

- Wages: $20,000

- Marketing & Supplies: $2,500

When you add them up, your total operating expenses come to $26,500 per month.

Overall, by calculating your operating costs, you can manage your budget and know whether your revenues can cover all the expenses to leave room for profit.

6. Prepare financial statements

After estimating your barbershop's revenue, COGS, and operating expenses, it’s time to draft clear financial statements. These documents are essential for illustrating your barbershop’s financial health and growth potential to prospective investors.

Here are the critical financial statements and reports that you should consider including in your plan:

- Income statement (profit and loss statement)

- Cash flow statement

- Balance sheet

- Break-even analysis

By adding these financial statements, you showcase your financial standing to potential investors so they can make well-informed decisions regarding investment.

We'll explore each of these financial components in greater detail in the upcoming sections, giving you the insights needed to create a strong financial plan.

7. Prepare visual reports

Numbers alone aren't enough. Present your barbershop’s financial data in a visually appealing and easily digestible format that readers can quickly understand and get valuable insights.

Using charts and graphs makes it easier to highlight your barbershop’s key aspects, including revenue trends, expenses, profit margins, and cash flow.

Don’t worry; it’s easy. Use simple bar charts, pie charts, and line graphs to make the data clear. Also, highlight patterns like seasonal sales changes or rising costs to help with planning.

This will not only help analyze financial data but also enable you to communicate key metrics effectively to your team as well as investors.

8. Test assumptions, consider scenario analysis

Finally, take a step back and test the numbers to ensure your projections are more accurate. Try to run different scenarios (best- and worst-case) to see how changes impact your financial outcomes.

For instance, consider what happens if product costs rise by 15% or client visits drop during slower months.

Considering these “what-if” situations helps you identify potential problems in business operations and come up with solutions in advance. It even increases transparency and lets investors better understand your barbershop’s future with different scenarios.

Overall, these test assumptions and sensitivity analysis will help you make strategic decisions and necessary adjustments to keep your barbershop running smoothly.

Key financial statements of a barbershop financial plan

A detailed barbershop financial plan typically includes important financial documents like the income statement, cash flow statement, balance sheet, and break-even analysis.

These reports clearly describe your barbershop's current monetary position and the overall financial strategy to achieve future goals.

Let's explore each statement in detail.

1. Income statement

The income statement is also known as the profit and loss statement. It gives you a solid understanding of your barbershop’s revenue, expenses, gross margin, and net profit for a specific time.

It helps you see whether your business is making enough money to cover its costs and turn a profit.

The gross profit is what you get after subtracting the COGS from the total revenue. This shows how efficiently your barbershop uses its resources.

Further, divide the gross profit by revenue and convert it into a percentage to determine the gross margin.

Then, reduce operating costs like rent, salary, and utility to get the EBITDA. Finally, subtract interest, taxes, depreciation, and amortization from the EBITDA to arrive at the net profit of your barbershop—the figure that investors care about the most.

Here’s an example of a mid-sized barbershop’s income statement to demonstrate these calculations:

| Category | Amount ($) |

|---|---|

| Revenue | |

| Haircuts & Styling | $85,000 |

| Beard Trimming | $15,000 |

| Product Sales (Shampoos, Gels, etc.) | $10,000 |

| Other Services (Shaves, Facials) | $5,000 |

| Total Revenue | $115,000 |

| Cost of Goods Sold (COGS) | |

| Cost of Products Sold | $4,000 |

| Barber Supplies (Razors, Clippers, Towels, etc.) | $6,000 |

| Total COGS | $10,000 |

| Gross Profit | $105,000 |

| Operating Expenses | |

| Rent | $18,000 |

| Utilities (Electricity, Water, Internet) | $4,500 |

| Salaries & Wages (Barbers, Staff) | $40,000 |

| Marketing & Advertising | $5,000 |

| Insurance | $2,500 |

| Equipment Maintenance | $3,000 |

| Miscellaneous Expenses | $2,000 |

| Total Operating Expenses | $75,000 |

| Operating Profit (EBIT) | $30,000 |

| Other Expenses | |

| Loan Interest | $2,000 |

| Depreciation | $3,000 |

| Total Other Expenses | $5,000 |

| Net Profit (Before Taxes) | $25,000 |

| Taxes (20%) | $5,000 |

| Net Profit (After Taxes) | $20,000 |

The barbershop pulls in $115,000 from haircuts, beard trims, product sales, and other services. Out of that, $10,000 goes toward supplies and products, leaving $105,000 in gross profit.

Then come the regular expenses—rent, salaries, utilities, and marketing—which add up to $75,000. After covering those, there’s $30,000 left.

On top of that, loan interest and depreciation cost another $5,000, bringing the profit down to $25,000 before taxes.

Once taxes take out another $5,000, the shop is left with $20,000 in profit.

In simple terms, the income statement tells you if your barbershop is making money and staying financially healthy over time.

2. Cash flow statement

A cash flow statement shows how money is coming in and going out of your barbershop over a certain period. It helps you figure out if you have enough cash to cover your daily expenses.

It’s also great for spotting potential cash shortages, especially during slower months, and demonstrates how much cash is coming from operations compared to things like investments or loans.

To create one, you’ll need to include cash from sales, costs like hair care products and supplies, and other overhead expenses. It highlights how much money your barbershop is making and spending during that period.

| Category | Amount ($) |

|---|---|

| Cash Flow from Operating Activities | |

| Net Profit (After Taxes) | $20,000 |

| Adjustments for Non-Cash Expenses: | |

| Depreciation | $3,000 |

| Changes in Working Capital: | |

| Increase in Accounts Receivable | ($2,000) |

| Increase in Inventory | ($1,500) |

| Increase in Accounts Payable | $2,500 |

| Net Cash from Operating Activities | $22,000 |

| Cash Flow from Investing Activities | |

| Purchase of Equipment | ($5,000) |

| Net Cash Used in Investing Activities | ($5,000) |

| Cash Flow from Financing Activities | |

| Loan Received | $10,000 |

| Loan Repayment | ($4,000) |

| Net Cash from Financing Activities | $6,000 |

| Net Increase in Cash | $23,000 |

| Beginning Cash Balance | $5,000 |

| Ending Cash Balance | $28,000 |

That said, it’s a good illustration of how well your business is at generating cash. The precision of your projections in these aspects directly impacts the reliability of your cash flow.

So, be realistic with the assumptions you make in the cash flow statement. Use industry standards and consider market situations to ensure accuracy.

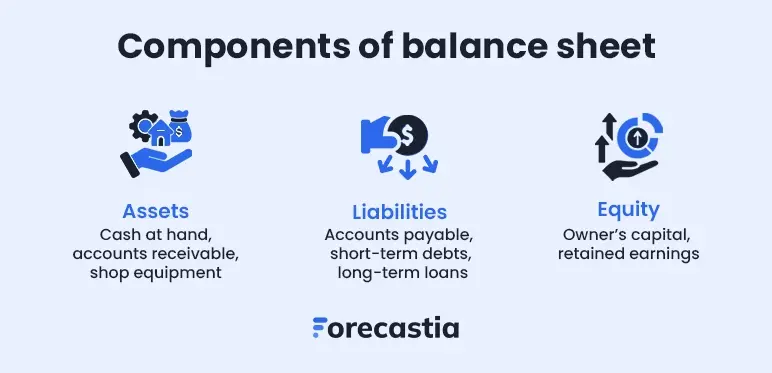

3. Balance sheet

A balance sheet gives a quick snapshot of your barbershop’s financial position for a specific timeframe. It shows what the barbershop owns, what it owes to others, and what’s left for you.

After all, it covers these 3 key elements: Assets, Liabilities, and Shareholders equity.

Ideally, it’s presented as, Assets = Liabilities + Equity.

| Category | Amount ($) |

|---|---|

| Assets | |

| Cash | $28,000 |

| Accounts Receivable | $2,000 |

| Inventory | $1,500 |

| Total Current Assets | $31,500 |

| Equipment | $15,000 |

| Less: Accumulated Depreciation | ($3,000) |

| Total Fixed Assets | $12,000 |

| Total Assets | $43,500 |

| Liabilities | |

| Accounts Payable | $2,500 |

| Short-term Loan Payable | $4,000 |

| Total Current Liabilities | $6,500 |

| Long-Term Loan Payable | $6,000 |

| Total Liabilities | $12,500 |

| Owner’s Equity | |

| Owner’s Investment | $11,000 |

| Retained Earnings | $20,000 |

| Total Equity | $31,000 |

| Total Liabilities & Equity | $43,500 |

Investors really pay close attention to the balance sheet because it shows them your barbershop’s financial structure, return on investment (ROI), and overall stability.

It also provides an idea of the cash that is available to you, how the money is blocked, and what kind of solid business you are running.

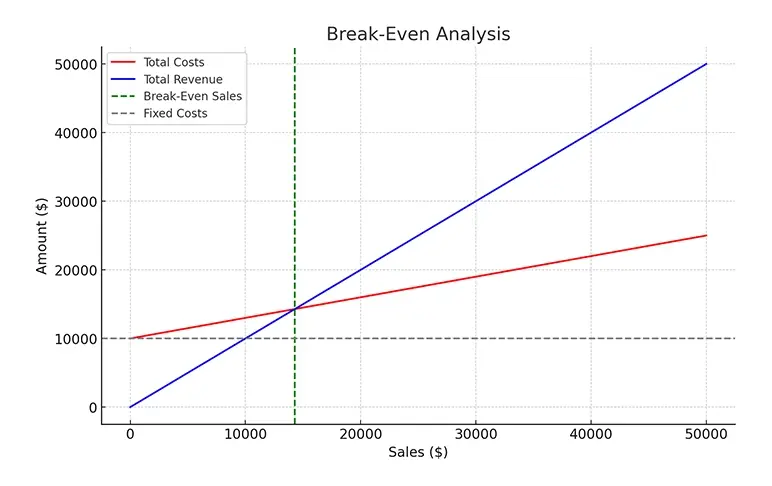

4. Break-even analysis

We all know that profit is the all-time motive of all barbershop owners. The real question is: When does the money actually start coming in?

A break-even analysis fits the bill at this stage. It shows exactly how much you’ll need to generate in revenue for all the costs to be recovered—no profit and no loss; just breaking even.

Let's take an example to see how it works.

For a quick-service barbershop:

Fixed costs: $10,000 (including rent, utilities, and wages)

Variable costs: $12,000

Revenue: $40,000

Contribution Margin: ($40,000 - $12,000) ÷ $40,000 = 0.70 (or else 70%)

Break-even Sales Calculation: $10,000 ÷ 0.70 = $14,285

This analysis shows exactly how much revenue is needed to reach the point where your total sales just cover your costs, causing no profit or loss.

In addition, this will give potential investors or lenders a fair idea of when your barbershop would be profitable.

Download free barbershop financial projections example

Creating a barbershop financial plan from scratch seems overwhelming. After all, Excel sheets are tiring and endlessly long. But no worries! We’re here to help you with our free barbershop financial plan sample.

It covers all the key components of a barbershop's financial projection, such as sales forecast, P&L or income statement, balance sheet, cash flows, and break-even analysis, simplifying the entire financial planning process to help you get started.

Build accurate financial projections using Forecastia

That’s it! We’ve discussed almost everything about creating barbershop financial projections in this guide. Now, it should be much easier for you to put that knowledge into action and start planning.

But if it still feels like a lot to handle, don’t worry; Forecastia is the only AI-powered financial forecasting tool you need to make the process simple and stress-free.

It’s specifically designed for businesses looking to build accurate financial projections, anticipate future cash flows, and analyze overall financial performance—all without using spreadsheets!

Frequently Asked Questions

What are the key financial statements in a barbershop financial plan?

A barbershop financial plan includes these essential financial statements:

- Income statement

- Cash flow statement

- Balance sheet

- Break-even analysis

What are common operating expenses in a barbershop financial plan?

Typical barbershop operating expenses include:

- Rent and utilities

- Supplies and products

- Labor costs

- Equipment maintenance

- Marketing and advertising

How often should I update my barbershop’s financial projections?

It’s best to review and update your financial plan every six months or when there are significant changes in your business, such as price adjustments, new services, or increased expenses.

How to use the barbershop financial projections template?

Enter your barbershop’s details, such as:

- Projected client traffic and average service price

- Cost of Goods Sold (COGS) for products used

- Operating expenses like rent, wages, and marketing

Templates usually include built-in formulas that help calculate profit margins, cash flow, and break-even points, letting you understand your barbershop’s financial health.

How do I create financial projections for my barbershop?

Follow these steps to create financial projections:

- Estimate monthly revenue based on the number of clients, average service price, and frequency of visits.

- Calculate fixed costs (rent, utilities, wages) and variable costs (products, commissions).

- Prepare income statements, cash flow reports, and balance sheets to track financial performance.

- Use what-if scenarios to test different situations, like seasonal slowdowns or price changes.

Follow Vinay Kevadiya